Collections leaders talk about recovery rates. Creditors talk about predictability. The gulf between those two conversations usually comes down to a single issue: whether there’s a portfolio segmentation collections strategy in place that actually holds up under mixed-risk conditions.

In three previous posts, we’ve examined the importance of results over activity, how to turn analytics into proof of performance, and why data recovery reporting consistency matters in client retention. Now let’s dig into why segmentation is so crucial.

Every agency manages mixed-risk debt

Every agency manages mixed-risk debt portfolios. Early-stage credit card delinquencies. Charged-off fintech accounts. Small-balance telecom receivables. High-balance personal loans. Healthcare balances with heightened compliance sensitivity.

At the macro level, the scale of consumer credit exposure underscores why segmentation discipline matters. According to the Federal Reserve Bank of New York, total U.S. household debt reached approximately $18.8 trillion in Q4 2025, with roughly 4.8% of outstanding debt delinquent at some stage.

When portfolios shift at that scale, small variations in risk handling compound quickly.

Additionally, the New York Fed reports that 4.6% of consumers had a third-party collection account in Q4 2025. Mixed-risk exposure isn’t theoretical, but embedded in the system.

Even so, many agencies still operate under the assumption that performance will naturally vary by debt type, and this kind of variance is acceptable.

Creditors disagree.

When recovery rates swing unpredictably between risk tiers, it signals inconsistent execution. When the enterprise is evaluating its collections vendors, volatility is interpreted as weak operating control.

This is where scalable collections performance management becomes more than a reporting exercise. It’s evidence of operational maturity.

The portfolio problem no one talks about

Agencies routinely accept large performance gaps between portfolio types. High-risk portfolios underperform. Low-risk portfolios overperform. Blended averages look fine.

But creditors don’t evaluate agencies on blended averages. They evaluate them on risk-adjusted stability.

Research from Experian shows that effective collections strategies segment cases “by exposure, risk and behavioral dimensions.” Risk is multi-variable. The delinquency stage alone is not enough.

Similarly, TransUnion reporting indicates that derogatory trades and delinquency growth are disproportionately concentrated in higher-risk tiers, and that these tiers deteriorate faster under stress. Risk bands do not move uniformly.

At the macro level, delinquency behavior also shifts over time. A Federal Reserve FEDS Note observed that credit card and auto loan delinquency rates began flattening in 2025 after prior increases. Portfolio mix changes create performance pressure even when collector effort remains constant.

Standardizing recovery rates across segments doesn’t mean forcing identical outcomes. It means controlling variability so that differences are explainable, forecastable, and bounded.

That distinction defines enterprise readiness.

Why risk diversity breaks traditional operating models

Mixed-risk debt portfolios expose weaknesses in human-dependent operating models.

Different segments require different treatment logic. Early-stage reminders require speed and minimal friction. Late-stage recovery requires structured negotiation. Medical debt requires higher sensitivity. Fintech charge-offs require balance-to-income awareness. Compliance expectations escalate with certain product types.

Collectors are forced to context-switch continuously. Improvisation fills the gaps.

Execution drift accumulates. Scripts evolve in practice. Negotiation approaches differ by collector. Escalation timing varies. Supervisors calibrate differently across teams.

Research from McKinsey & Company on operating models shows that organizations frequently experience a significant gap between strategy design and execution, with performance variance stemming from inconsistent operating discipline.

In collections, risk diversity magnifies this effect. The more heterogeneous the portfolio, the more inconsistent performance becomes.

Portfolio mix volatility reinforces this challenge. The St. Louis Federal Reserve’s FRED series on credit card delinquency shows measurable fluctuations across quarters. Even small percentage shifts materially alter risk-weighted outcomes.

Training reduces variance temporarily. Turnover reintroduces it. Portfolio composition changes amplify it.

Standardizing outcomes requires system-level enforcement. Operational transformation like this isn’t easy: according to McKinsey, 63% of enterprises meet most transformation objectives but only 24% are “highly successful.” But in the collections industry, achieving this level of transformation provides potent differentiation from agency competitors vying for your clients.

Segmenting portfolios the right way

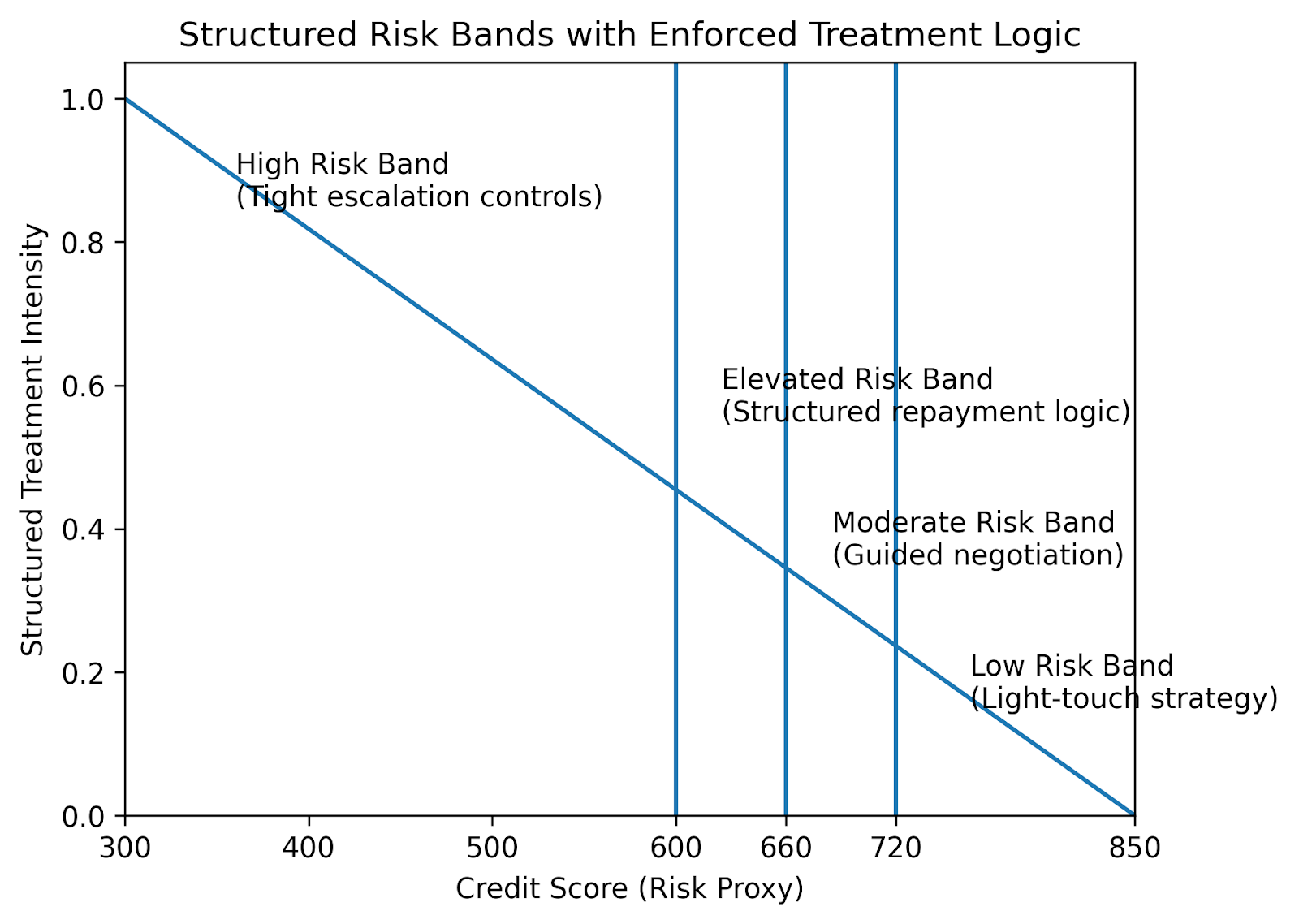

Portfolio segmentation collections strategy often relies on blunt categories: early vs. late stage, prime vs. subprime, small vs. large balance.

As we’ve seen, that isn’t enough. Effective collections segmentation strategy operates on structured risk bands combining credit risk, balance size, delinquency stage, payment history, channel responsiveness, and compliance sensitivity.

TransUnion’s CIIR data shows divergence across super prime, prime, near-prime, and subprime tiers, reinforcing that recovery strategies cannot be uniform across risk profiles.

Risk bands create controlled treatment paths.

Low-risk accounts may prioritize frictionless digital payment. Mid-risk accounts may require guided negotiation boundaries. High-risk accounts may require structured repayment plans and stricter compliance scripting.

Segmentation must be enforced, not suggested. Regulatory expectations reinforce this need. The Consumer Financial Protection Bureau debt collection rule establishes call-frequency presumptions and disclosure standards that vary by communication channel.

Additionally, CFPB compliance guidance clarifies that federal rules do not preempt stricter state law limits. Portfolio rules must be configurable and auditable at the state and client level.

The takeaway? Segmentation is both a performance strategy and a compliance safeguard.

AI as a standardization layer

Standardizing recovery rates across mixed-risk debt portfolios requires a logic layer that executes consistently.

AI-driven systems, when properly architected, encode portfolio-specific rules into goal-driven treatment strategies.

Within a properly designed framework, voice-first AI agents are operating under defined business logic. Conversations are structured around payment objectives, compliance constraints, and portfolio-defined boundaries.

Risk-band-specific negotiation ranges are enforced automatically. Escalation triggers activate based on data thresholds rather than collector discretion. Contact frequency limits are embedded and auditable in accordance with CFPB standards.

This prevents collector improvisation from distorting outcomes. AI becomes a standardization layer rather than a volume multiplier. And we’ve just seen the value of standardization.

Volume without this level of control amplifies variance. Logic with enforcement compresses it.

Measuring success across risk profiles

Standardizing outcomes doesn’t mean reporting a single blended recovery rate.

It requires normalized performance benchmarks such as recovery rate by risk band, promise-to-pay conversion by delinquency stage, average days to resolution by balance tier, complaint ratio by segment, and variance range across comparable portfolios.

Enterprise buyers increasingly request dispersion metrics.

Given the increases in consumer debt (and delinquency), creditors are scrutinizing performance volatility more closely. And subprime delinquency rates can move independently of overall averages. Blended reporting masks this divergence.

Scalable collections performance management answers three questions clearly:

- How does each risk band perform?

- How stable is that performance quarter over quarter?

- What happens when portfolio composition changes?

If those answers depend on individual collectors, your model is fragile. If they depend on embedded logic and structured segmentation, your model is resilient.

How Overtime standardizes performance across mixed-risk portfolios

Overtime was built specifically to address performance dispersion across mixed-risk debt portfolios. Our voice-first AI agents operate within enforced, risk-band-specific logic rather than generalized automation. Each portfolio segment can be configured with defined negotiation parameters, timing rules, escalation triggers, compliance disclosures, and contact cadence limits. That logic is executed deterministically at scale.

Because treatment strategies are embedded into the platform, collectors aren’t improvising across segments. Performance becomes structured and auditable. Recovery rates can be analyzed by normalized risk band rather than blended averages, enabling agencies to demonstrate controlled variability to creditors.

Overtime’s built-in compliance guardrails align with CFPB regulatory expectations while maintaining consistent tone and treatment standards. Real-time analytics track dispersion across segments, allowing agencies to forecast performance ranges under portfolio mix changes.

The result? Standardized recovery performance that remains stable even as risk profiles shift, without expanding headcount or increasing operational volatility.

Benefits of Performance Standardization Across Risk Bands

Scale requires discipline, not just technology

Mixed-risk debt portfolios are expanding in complexity as consumer credit grows and shifts.

Agencies that rely solely on human adaptation or off-the-shelf workflow platforms will struggle to maintain stable recovery rates across segments.

Portfolio segmentation collections strategy must evolve from descriptive to enforced.

Standardizing recovery rates across risk profiles does not flatten outcomes. It builds structured risk bands, embeds portfolio-specific logic, and measures normalized performance rigorously.

Enterprise buyers evaluate stability under complexity, and standardization is the backbone of how you prove it.